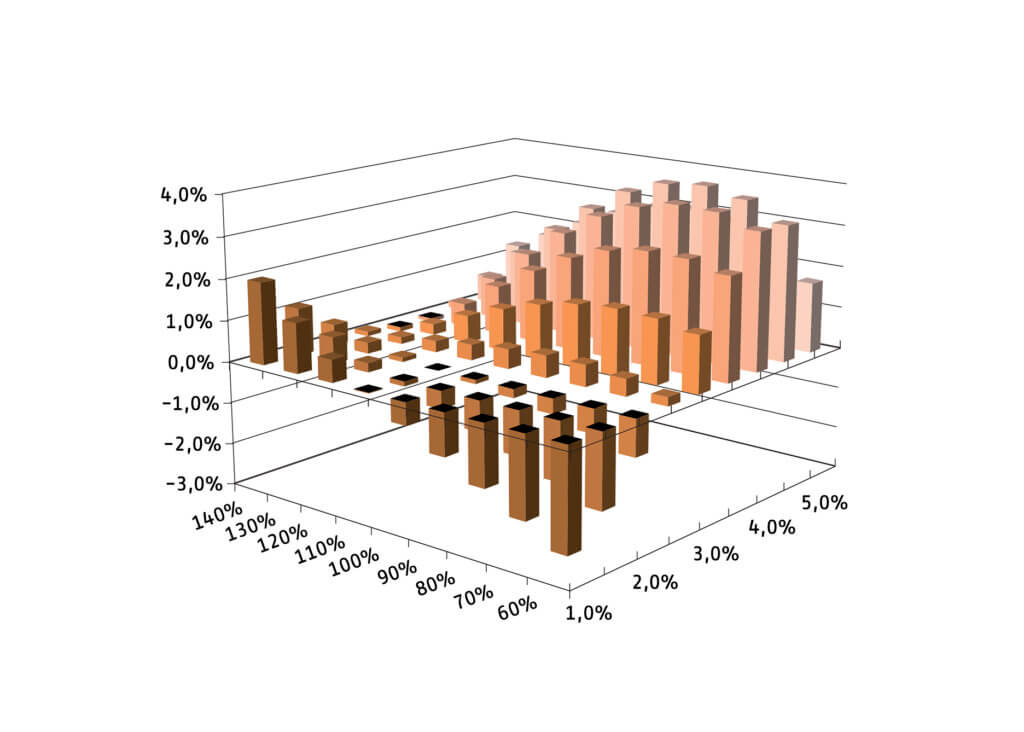

Use of Solvency II’s volatility adjustment (VA) causes hard-to-explain movements in own funds and perverse incentives for hedging and risk management. In this paper, Richard Plat proposes an alternative approach to solve these issues.

Use of Solvency II’s volatility adjustment (VA) causes hard-to-explain movements in own funds and perverse incentives for hedging and risk management. In this paper, Richard Plat proposes an alternative approach to solve these issues.