Government bonds constitute a substantial portion of Dutch insurers’ investment portfolios.1 Primarily used for liability-matching, Eurozone sovereign bonds have long been favoured for their perceived safety, stability and low capital requirements under Solvency II. However, recent developments in sovereign bond markets—marked by widening spreads, rising yields, and persistent fiscal deficits—suggest that this perception may require reassessment.

In this article, we examine the evolving dynamics of sovereign yields and credit spreads in the context of government budgetary trends. We explore the implications of rising sovereign credit risk for insurers, focusing on both quantitative modelling and practical portfolio management considerations.

Historical Perspective

The historical evolution of European and U.S. sovereign bond yields is illustrated in the figure below. Figure 1: Historical 10-year government bond yields (Eurozone and US).2

The figure points to multiple sovereign yield (and spread) regimes that have been observed in the past and were extensively analysed and discussed.

Figure 1: Historical 10-year government bond yields (Eurozone and US).2

The figure points to multiple sovereign yield (and spread) regimes that have been observed in the past and were extensively analysed and discussed.

- The high-rate environment of the 1970s and early 1980s, following the collapse of the Bretton Woods system. This period was marked by oil shocks, stagflation, and aggressive monetary tightening.

- The onset of the Great Moderation in the mid-1980s, characterized by fiscal and monetary stabilization and a gradual decline in yields throughout the 1990s.

- The convergence of Eurozone sovereign yields in the lead-up to and aftermath of the euro’s introduction in the late 1990s and early 2000s.

- The Global Financial Crisis, Great Recession, and Eurozone Sovereign Crisis, during which government bond yields spiked sharply due to mounting fiscal pressures and concerns over debt sustainability in several member states. While central banks intervened with aggressive monetary easing, yield spreads (vs. swap) widened as markets began to reprice sovereign risk. Simultaneously, a pronounced flight to quality was observed, with yields on high-rated sovereigns (e.g., U.S., Germany, Netherlands) falling sharply—many into negative territory.

- The COVID-19 shock, which once again triggered significant fiscal expansion and a subsequent rise in sovereign yields.

Figure 2: General government debt as percentage of GDP.3

With the exception of Italy—and to a lesser extent, Belgium—most EU member states and the U.S. maintained relatively sustainable debt-to-GDP ratios for much of the historical period. However, the aftermath of the 2008 Global Financial Crisis, including the Eurozone Sovereign Crisis, led to a marked deterioration in fiscal positions. While some countries managed to stabilize their debt trajectories, the broader post-2008 trend has been one of rising deficits. This was further amplified by the expansive fiscal response to the COVID-19 pandemic, which caused sharp—albeit temporary—increases in public debt levels.

Figure 2: General government debt as percentage of GDP.3

With the exception of Italy—and to a lesser extent, Belgium—most EU member states and the U.S. maintained relatively sustainable debt-to-GDP ratios for much of the historical period. However, the aftermath of the 2008 Global Financial Crisis, including the Eurozone Sovereign Crisis, led to a marked deterioration in fiscal positions. While some countries managed to stabilize their debt trajectories, the broader post-2008 trend has been one of rising deficits. This was further amplified by the expansive fiscal response to the COVID-19 pandemic, which caused sharp—albeit temporary—increases in public debt levels.

Post-Covid Trends

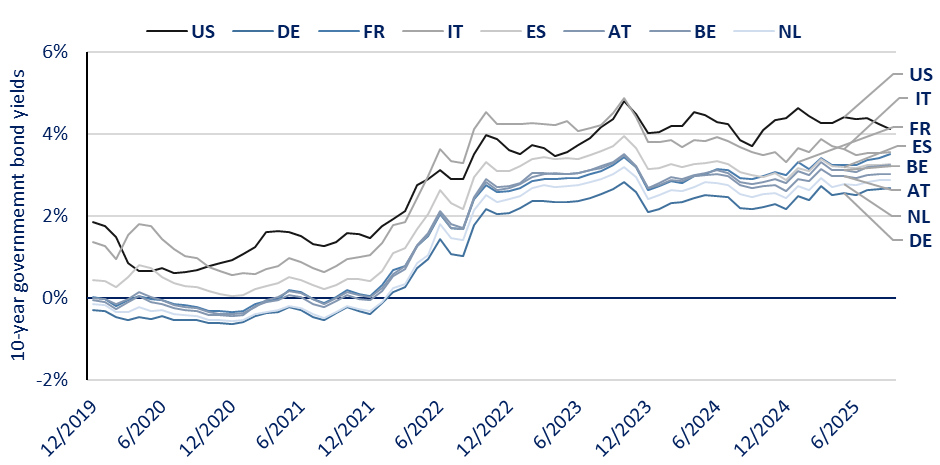

The strong fiscal and monetary response to the COVID-19 outbreak led to a significant expansion of the monetary base and a sharp increase in government spending. While these measures helped cushion the economic fallout—allowing GDP to rebound relatively quickly—they also placed mounting pressure on public finances. The inflation surge of 2021–2022, partly driven by the Energy Crisis, prompted central banks to tighten monetary policy. As a result, government bond yields rose markedly, as illustrated in the figure below. Figure 3: 10-year government bond yields (Eurozone and US) (2019–2025).4

Although these elevated yields do not represent historical extremes (see Figure 1), they follow an extended period of ultra-low or even negative interest rates. Crucially, this rise in borrowing costs has occurred at a time of persistently high government deficits—stemming from pandemic-related spending and subsequent responses to the energy and cost-of-living crises.

This fiscal strain was compounded by sluggish economic growth across many advanced economies, with forecasts for several countries remaining subdued. Higher interest rates are likely to weigh further on growth prospects. The risk of stagflation is amplified by political uncertainty and potential spillovers from U.S. trade policy, including the reintroduction of tariffs. While the U.S. Federal Reserve initiated a modest rate cut of 25 basis points in October 2025, central banks are expected to proceed cautiously with further easing.

In this environment, governments may increasingly confront the adverse implications of the “g vs. r” dynamic—where the economic growth rate (“g”) remains structurally below the interest rate on public debt (“r”). This imbalance raises concerns about long-term debt sustainability, especially in the context of high debt-servicing costs, weak growth, and constrained fiscal space. In the event of future real-economy shocks, governments may find their capacity to respond significantly diminished. Moreover, the risk of adverse feedback loops—where market or economic stress triggers sovereign credit deterioration—has become more pronounced.

These concerns have been reflected in market sentiment. Sovereign bond spreads (relative to swaps) have widened steadily over the past two years, driven by fears of fiscal cliffs, political instability, and weak growth trajectories. Rating agencies have responded accordingly: in October 2025, Moody’s downgraded France’s sovereign rating to Aa3, while Austria and Belgium also saw rating downgrades earlier in the year. While U.S. Treasuries remain relatively insulated—owing to their dominant role in global finance and the Federal Reserve’s credibility—individual Eurozone sovereigns face more acute challenges in sustaining investor demand.

For insurers, the resulting volatility in sovereign credit markets carries significant implications. With government bonds comprising a substantial share of their balance sheets, rising spreads and rating downgrades may affect both capital requirements and asset-liability management strategies.

Figure 3: 10-year government bond yields (Eurozone and US) (2019–2025).4

Although these elevated yields do not represent historical extremes (see Figure 1), they follow an extended period of ultra-low or even negative interest rates. Crucially, this rise in borrowing costs has occurred at a time of persistently high government deficits—stemming from pandemic-related spending and subsequent responses to the energy and cost-of-living crises.

This fiscal strain was compounded by sluggish economic growth across many advanced economies, with forecasts for several countries remaining subdued. Higher interest rates are likely to weigh further on growth prospects. The risk of stagflation is amplified by political uncertainty and potential spillovers from U.S. trade policy, including the reintroduction of tariffs. While the U.S. Federal Reserve initiated a modest rate cut of 25 basis points in October 2025, central banks are expected to proceed cautiously with further easing.

In this environment, governments may increasingly confront the adverse implications of the “g vs. r” dynamic—where the economic growth rate (“g”) remains structurally below the interest rate on public debt (“r”). This imbalance raises concerns about long-term debt sustainability, especially in the context of high debt-servicing costs, weak growth, and constrained fiscal space. In the event of future real-economy shocks, governments may find their capacity to respond significantly diminished. Moreover, the risk of adverse feedback loops—where market or economic stress triggers sovereign credit deterioration—has become more pronounced.

These concerns have been reflected in market sentiment. Sovereign bond spreads (relative to swaps) have widened steadily over the past two years, driven by fears of fiscal cliffs, political instability, and weak growth trajectories. Rating agencies have responded accordingly: in October 2025, Moody’s downgraded France’s sovereign rating to Aa3, while Austria and Belgium also saw rating downgrades earlier in the year. While U.S. Treasuries remain relatively insulated—owing to their dominant role in global finance and the Federal Reserve’s credibility—individual Eurozone sovereigns face more acute challenges in sustaining investor demand.

For insurers, the resulting volatility in sovereign credit markets carries significant implications. With government bonds comprising a substantial share of their balance sheets, rising spreads and rating downgrades may affect both capital requirements and asset-liability management strategies.

Potential Impacts on the Insurance Sector

The evolving risk profile of sovereign bonds has implications for insurers across multiple dimensions—from investment strategy and risk management to regulatory and internal model calibration. Given the sector’s substantial exposure to Eurozone and U.S. sovereign issuers, these developments warrant close attention. Government bonds play a central role in insurers’ portfolios, serving both as collateral and as instruments for asset-liability management (ALM). The recent rise in sovereign yields has arguably improved their attractiveness from a capital-efficiency and return perspective. Moreover, the upcoming implementation of EIOPA’s Solvency II 2020 review encourages insurers to enhance credit-risk sensitivity to optimize the volatility adjustment mechanism. These incentives, combined with ALM needs, typically favour longer-duration holdings. From a modelling standpoint, the Standard Formula under Solvency II continues to apply a 0% capital charge to Euro-denominated sovereign bonds. However, insurers using (partial) internal models must regularly update their calibrations for spread, default, and migration risks. This includes incorporating observed spread movements and rating changes. Beyond the 1-year stress horizon mandated by Solvency II, multi-year real-world projections may also need to be revisited in light of shifting risk-return expectations. Below are some of the areas where insurers may be particularly exposed to rising sovereign credit risk: Volatility of Valuations- Elevated sovereign risk translates into more frequent and potentially more severe price fluctuations. Political instability and market overreaction can amplify these swings.

- Insurers may not fully benefit from the offsetting widening of the volatility adjustment, especially if their portfolios diverge from EIOPA’s reference portfolio composition. Longer-duration bonds are more sensitive to spread changes, increasing valuation risk.

- Hedging strategies may offer partial mitigation, but protection costs can be high and availability limited (for some issuers/issues).

- The limited pool of Eurozone sovereign issuers and their shared exposure to systemic risks heightens concentration risk. Rating downgrades may trigger portfolio rebalancing, constrained by exposure limits per rating bucket.

- In a sovereign credit shock, AAA-rated issuers (e.g., Germany, Netherlands) may still serve as safe havens—but the flight-to-quality effect could be weaker than in the past crises, thereby further reducing the potential for diversification.

- Interconnectedness among Eurozone economies increases the likelihood of contagion dynamics.

- Current spread risk calibrations are largely based on the 2008–2009 and Eurozone Sovereign Crisis periods. Recent spread increases have unfolded gradually, not as (1-year) tail events, but may still influence annual volatility estimates and shock distributions (in particular for the less extreme tails).

- Market sensitivity to adverse news could lead to temporary spread surges, challenging the prudency of existing calibrations.

- Migration risk assumptions, also rooted in past crises, may need updating to reflect recent downgrades and evolving macroeconomic conditions.

- Dependencies between sovereign credit risk and other market factors may require reassessment.

- Unlike past crises, recent spread widening has coincided with rising swap rates (especially in 2021-2022).

- Country-specific risk profiles have shifted, potentially altering the relationship between rating migration and spread dynamics. Assumptions around safe haven behaviour may need to be revisited; while flight-to-quality effect remains a plausible assumption in principle, its magnitude and consistency may differ.

- Many considerations from 1-year capital modelling also apply to long-term economic scenarios.

- Yield and spread expectations may need re-evaluation, incorporating both quantitative and qualitative insights.

- The probability of extreme shocks over the projection horizon should be benchmarked against broader market expectations.

- It may need to be assessed whether yield/spread convergence or divergence across countries and/or ratings is more likely, including potential structural breaks and mean-reverting behaviour.

- Rating migration modelling may also require updated assumptions to reflect recent trends.